Here at SB&D, we try to stick to the data and the analysis. That is difficult to do when the data is so. . .what word am I trying to grasp here. . .“conflicting.” The economic data appears “conflicting” because different parts of the economy are moving in opposite directions.

For example:

GDP data is decent if not good. And in Q3 of 2025, it was absolutely great — an annualized rate of 4.4 percent, much higher than any quarter in 2025. Q4 fell to 0.7 percent.

1a: There were more mass layoffs in 2025 than any year since the recession-ravaged year of 2009 (sans COVID).

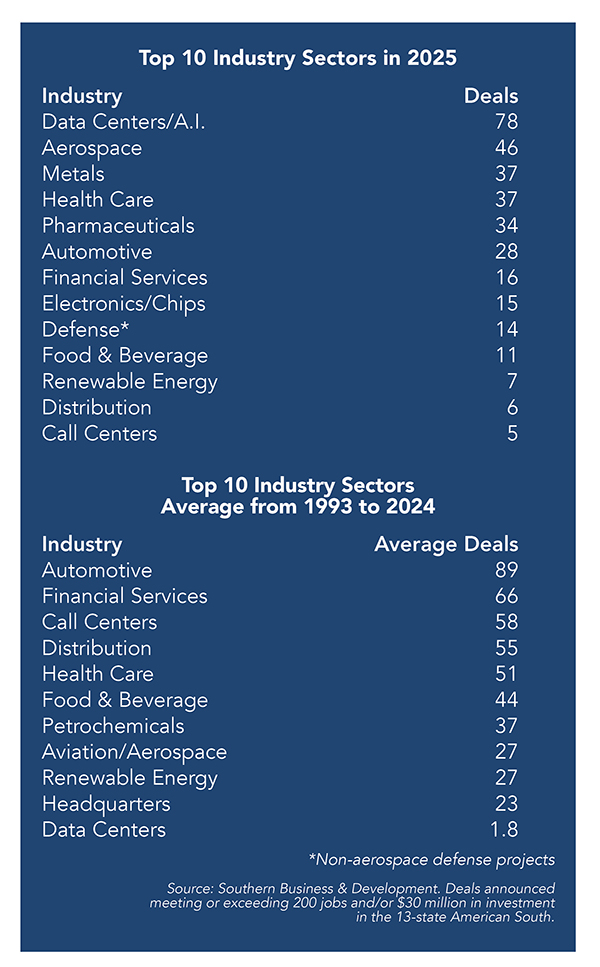

1b: At the same time, private sector job creation is totally stagnant throughout the U.S., states in the South included. In February, we lost 92,000 jobs. Artificial intelligence/data centers are the only game in town in 2025 (other than aerospace, health care and metals), when it comes to deals in the South.

2a: Automotive and financial services, the absolute, fundamental bedrock of the South’s economy, faltered in project announcements last year as automotive deals dropped by almost 70 percent from normal levels. In 2025, those two industries saw the least number of job and investment announcements since the Great Recession.

Those two industries are the largest job generators almost each and every year outside of health care in the American South. Both have been bellwethers or the canary in the coal mine of the South’s and America’s economy for 100-plus years. When automotive and financial services slow their deals, our 40-plus years of experience tell us that a recession is either here or right around the corner. Then again, with such conflicting data, we are not quite sure that still applies.

A.I. has helped increase worker productivity to levels not seen in decades with a 4.9 percent increase in Q3 2025, and a 2.8 percent increase in Q4 2025. This surge was driven by a 5.4 percent increase in output, which outpaced a 0.5 percent increase in hours worked. Since 1947, the average annual worker productivity rate is 2.1 percent according to the Bureau of Labor Statistics.

However, experts say A.I. productivity gains show up unevenly in data. As for me, not true. A.I. is an astounding tool for journalists because research time for an article like this one has been cut in my estimation by about 65 percent.

The stock market was setting records, until we bombed Iran. The affluent are propping up services, such as retail and travel.

4a: On a micro level, my brother-in-law, Don Murdoch, owns the best independent music shop in the South in Birmingham, Ala. He has owned it for over 40 years. In fact, we both started our businesses in the same year in the early 1980s as twenty-something’s and in the same town. I founded and launched the Birmingham Business Journal and he launched Highland Music in the same year.

4a: On a micro level, my brother-in-law, Don Murdoch, owns the best independent music shop in the South in Birmingham, Ala. He has owned it for over 40 years. In fact, we both started our businesses in the same year in the early 1980s as twenty-something’s and in the same town. I founded and launched the Birmingham Business Journal and he launched Highland Music in the same year.

All kinds of musicians, such as Billy Gibbons (ZZ Top), The War on Drugs and others visit his shop when they are in Birmingham to buy famous, new and old guitars and equipment.

Don told me around Christmas when I asked, “In this economy, who is buying guitars at your shop?” Don said, “No one is buying the cheap stuff. It’s all rich people buying expensive guitars.”

4b: Those who do not own stocks are struggling with high inflation, rent and other rising costs.

4c: In fact, a Lending Tree survey shows that 37 percent of Americans reported being behind on at least one monthly bill in 2025 (credit cards, rent, utilities) when in calendar year 2023, that figure was 11.7 percent, according to the FDIC. Again, the rich are getting richer and the poor, poorer.

Dr. Walter Kemmsies, Ph.D., Chief Economist of the Kemmsies Group (Savannah, Ga.), a veteran of our Southern Economic Development Roundtable@RosemaryBeach, said this in December at SEDR: “Consumer spending fuel is waning. Payment delinquency rates have risen significantly in the last few years. A near term recession is likely even without cuts to federal government spending and employment.”

Dr. Walter Kemmsies, Ph.D., Chief Economist of the Kemmsies Group (Savannah, Ga.), a veteran of our Southern Economic Development Roundtable@RosemaryBeach, said this in December at SEDR: “Consumer spending fuel is waning. Payment delinquency rates have risen significantly in the last few years. A near term recession is likely even without cuts to federal government spending and employment.”

Then in January when I called him, his tone was somewhat less certain as I asked him if he stood by his statements at SEDR about a likely recession. “Michael, if we have a recession, it would be a garden variety type like in 1990-1991, not like the Great Recession of 2007-2009.” Believe me, Walter knows, as the federal government contracts him and has for decades for his data.

4d: Manufacturing, real estate and retail are struggling with high costs and shifting demand. New and expanded manufacturing projects for 2025 in the South are down significantly. One of the reasons behind the struggles for businesses is that many are still eating the added costs of the tariffs. That’s not sustainable.

Baby Boomer retirements are reducing labor participation rates by millions each year.

5a: Labor participation rates in some Southern states are as high as 40 percent. That is according to the greats Neal Wade and Ed Castile at SEDR in December (look them up).

My uncle, Robert Lawler, told SEDR attendees recently that once folks get on disability, it is a rare case when one gets off it and gets back to work. He essentially told the group in 2025, “Once one gets on disability, they are on it for good.” Robert owned his own disability case management company for decades.

5b: The U.S. is currently experiencing a non-immigration economy, a policy that cannot resupply labor shortages as a result of some of the lowest birth rates in U.S. history. We predicted that in 2012. It’s not politics; it’s math.

5c: The U.S. still does not have a comprehensive immigration policy. It desperately needs one; one that vets every individual in an effort to find the best to come here.

So, let’s just move to this year’s SB&D 100 data and analysis, shall we?

Last year’s SB&D 100 batch of announced “Big Kahunas” (large corporate and industrial job and investment announcements, new and expanded) in the South will be noted as a deviation or divergence, if you will, from the norm of 33 years of data from the SB&D 100.

It’s a year that has never been duplicated and probably never will be as the support for A.I. and data centers in terms of construction, construction employment and capital investments are similar if not greater than the massive investments made from 2021 to 2024 in electric vehicle production and parts, specifically batteries.

Then again, 2026 may continue the string of data centers commanding the big deal list here in the world’s third largest economy. By all accounts, this data center boom will continue based on the demand of nearly $350 billion (that’s with a “B”) invested in the South in announced — not yet built for most —

data centers and artificial intelligence going forward. In fact, projections say that $350 billion invested in data centers in the South in 2025 may just be a drop in the bucket.

Truly, with no exaggeration, one industry dominated in 2025 — A.I. and its supporting data centers. And unlike past years, or decades, that domination wasn’t from the automotive or financial services sectors, the two largest industry sectors that have made the South rich for four decades or more.

Editor’s Note: The only industry since the first SB&D 100 was first published in 1994 (1993 data) that competed with automotive and financial services in total number of deals were those pesky call centers, which have averaged 58 deals of 200 jobs or more over the last 33 years. Now, if you go back prior to 1993, you could add chicken plants, apparel and textiles to that list. No more.

Editor’s Note: The only industry since the first SB&D 100 was first published in 1994 (1993 data) that competed with automotive and financial services in total number of deals were those pesky call centers, which have averaged 58 deals of 200 jobs or more over the last 33 years. Now, if you go back prior to 1993, you could add chicken plants, apparel and textiles to that list. No more.

Now, add call centers to apparel, textiles and coal as industries that are fundamentally gone and never to return, except for high-end apparel. The South got rich off those industries as well from the 1930s to the early 1990s. (Or rich for us at the time in the region’s rural areas.)

Then again, maybe we didn’t get rich because those industries were notorious for low pay. But for decades, that’s all the South had — sans farming — in addition to timber, which is still very active in the region. The South’s economy had to start somewhere post-Civil War and pre-WWI and WWII.

A tiny example of A.I.

A.I. has essentially wiped out call center announcements in the South and even the very existence of the industry itself. We counted five call center deals in 2025. I bet you there are none in 2026 of 200 jobs or more.

I mean, with A.I. why would there be? Even my local BBQ joint uses A.I. now for my phone-in order. You can ask it any question you want, like “I would like the ribs sliced please.” The answer from the A.I. “server:” “We will have them sliced for you Mr. Randle (I never gave ‘it’ my name). What time are you going to pick them up?”

Me: “Can you cut half a pie with the order?” “Artificial Annie” replies: “Of course, Mr. Randle. What flavor pie would you like to be cut in half?”

The oldest BBQ joint in Alabama, Golden Rule, “can add that to your order.” Golden Rule BBQ has been at its same location in the Birmingham suburb of Irondale since 1891.

The Rules?

Ah, “RULES” in an age when the rules are whatever humans (particularly politicos) make them out to be while they still can as A.I. will reset all rules each year going forward. Artificial intelligence is already smarter than us and way smarter than politicians.

And why not break the rules of economic development and the economy at large? The whole world is breaking all the geopolitical rules, especially the U.S. You can bet on that, as A.I. is an incredible “rule” and a journalist’s greatest tool ever, maybe since the dictionary.

As written earlier, my research time for articles like this has been cut by over 60 percent. It makes me more productive to go out and do more stuff, like selling advertisements for the new SouthernBusiness.com (summer), as this is our second-to-last print edition.

And A.I. is happening on the factory floor as well as in the shiniest office towers in Atlanta, Charlotte or Austin, as we now know.

Look, A.I. and “automation” are two different things altogether now. A.I. is directing our automation by accessing billions if not hundreds-of-billions of sources. The old Google couldn’t do that. That was a human job just a few years ago via whatever software chosen; software designed by humans.

A.I.: A gigantic boost in worker productivity

A.I.: A gigantic boost in worker productivity

The latest official data, released on January 8, 2026, show that U.S. non-farm labor productivity increased at a strong 4.9 percent annualized rate in the third quarter of 2025. That is basically unheard of. The data reflects the period from July through September 2025.

I know an economist who ranks “workforce productivity” as the most important factor in our economy. His name is Dr. Nariman Behravesh. I met and worked with him through Jim Newsome, former CEO of South Carolina Ports, as well as Dr. Kemmsies at the South Carolina International Trade Conference where we presented with my old nemesis, Wilbur Ross, the former U.S. Commerce Secretary during Trump’s first term.

Behravesh is retired now, but was Chief Economist of IHS Markit and author of Spin-Free Economics: A No-Nonsense, Nonpartisan Guide to Today’s Global Economic Debates (McGraw-Hill).

We are always in search of non-political geniuses to add to our work content. If it smells political, we throw it back like a bonito or ladyfish here in the South and that has been the case for five decades now.

Like Dr. Walter Kemmsies and Mark Vitner, Behravesh has no political leans. Like us, they just count this stuff up and with their vast experience, provide analysis.

Little did we know, though, a 4.9 percent increase in worker productivity would be at the expense of so many workers getting fired. Like over a million of them in one year, with new jobs a fraction of that figure in 2025.

Many economists predicted it, but many of us refused to believe it because some of the very CEOs that said “A.I. will not steal jobs,” are the ones laying off the most. Workers being replaced by machines will continue.

Regarding productivity, Mark Vitner, former senior economist at Wells Fargo and chief economist at Charlotte-based Piedmont Crescent Capital, had this to say regarding the rise in worker productivity since A.I. has come onto the scene as well as how the economic development layout has evolved:

Regarding productivity, Mark Vitner, former senior economist at Wells Fargo and chief economist at Charlotte-based Piedmont Crescent Capital, had this to say regarding the rise in worker productivity since A.I. has come onto the scene as well as how the economic development layout has evolved:

“Economic development has flipped the script, almost as abruptly as RFK Jr. flipped the food pyramid. After decades of engineering the economy for sugar highs, this cycle is being built on protein — capital spending directed toward long-cycle assets such as data centers, energy infrastructure, pharmaceuticals, and aerospace and defense. These sectors are capital-intensive by design: enormous dollar investments, relatively modest job creation, and outsized gains in productive capacity.

“The result is an economy increasingly driven by productivity rather than headcount — one capable of sustaining growth near 3 percent this year even as inflation continues to decelerate toward the Fed’s 2 percent target. By contrast, consumer-oriented investment has shifted into the slow lane, as capital gravitates toward higher-productivity, higher-return activities.”

So, again, we are just in the beginning of this massive uptick in productivity, the shining light in what is a bad omen for the traditional Southern economy. Then again, why are financial services struggling? That to me is the ultimate question in today’s economy.

You cannot bypass that bad omen. Just follow the money to know that financial services were not in a spending mood in calendar year 2025.

Traditional industries are slowing

Regardless, both of the South’s largest deal-making sectors had poor years last calendar year, with automotive posting just 28 deals meeting or exceeding SB&D 100’s thresholds. The yearly average since 1993 in automotive deals is 89 projects announced meeting or exceeding 200 jobs and/or $30 million in investment. That figure soared to 111 in 2015.

Financial services had their worst year since 2008 and 2009. They put up a mere 16 deals in 2025 (there were only five in the Great Recession year of 2008 when banks were closing left and right) when they averaged 66 big deals in the South each year since 1993.

Yup, “The Times They Are a-Changin’” (Bob Dylan, The Byrd’s, 1960s).

Then again, aerospace, aviation and defense in the South were as hot as automotive and financials were not in 2025.

Financial services didn’t make an annual contribution like it did 30, 20 or even five years ago. And automotive, if anything, is struggling through tariffs, a bubble from the EV division and a general forced modification in the worldwide supply chain.

Dr. Kemmsies told us in December that 86 percent of industrial manufacturing and 90-plus percent of automotive manufacturers are restructuring their supply chains. Those stats are historically highs, I would imagine.

Automotive, depending on who you talk to, is either at a tipping point, or not. Like all of calendar year 2025, many of the automotive CEOs simply did not know what to do, except back out on some of their EV deals, but most have simply been delayed.

Automotive had a decent year in vehicle sales in 2025, propped up again by the affluent and their ability to buy high-end vehicles. That sector just didn’t perform in new investments last year; again, an economy moving in opposite directions; a dichotomy.

A Double Bubble?

A Double Bubble?

But we now know this: The $250 billion spent on EV battery sites in the Southern Automotive Corridor from 2021 to 2024 is currently a bubble as more than half of those battery plants have been delayed, repurposed or, with one or two, closed as of January 2026. There are several $5 billion announced plants in the EV industry now built, but sitting vacant.

The great EV industry captures of 2021 to 2024 were simply too much, too fast. Then again, the federal incentives for green projects (Inflation Reduction Act of 2022) had a tight window to make a decision to invest.

Folks like Ford, Toyota and Hyundai, to name the most active, invested billions to gain those lucrative federal incentives in EV-related deals. Only for some CEOs to say later, “So, why did we do this so fast?”

It was a similar refrain heard back in 2010, when the U.S. became much more competitive with China as a result of rising wages there, some of my CEO friends said this regarding reshoring: “So, why are we making things halfway around the world for U.S. consumption?” It was a sound inquiry.

However, General Motors CEO Mary Barra told Reuters during a media event at the new GM Headquarters in Detroit, Mich., on January 12, 2026, that “We had to make some fairly significant changes,” referring to decisions to cut billions of dollars’ worth of EV investments while making a larger commitment to combustion-engine vehicles and hybrids. She also said, EVs are still the “end game” despite industry pullback in 2025.

It will be interesting to see this year if there are clawbacks from the feds and the states regarding those delayed and closed battery plants that have not churned out any product since completion, or, for that matter, housed any employees.

It is all up to demand, isn’t it? Like with every economic development gamble, right?

But now, the stakes are even higher with A.I. The question that arises is, “Could A.I. be walking the same path as EVs?” If so, we are in a world of hurt because with EV in a bubble and if A.I./data centers become a bubble, then we are in a “Dubble Bubble.”

Huge deviation from the norm as the rules have changed

We have never used the word “uncertain” so many times in our work. In prior deviations from the norm, most notably the dot-com era of the late 1990s, the war years of the early 2000s, the Great Recession late in the first decade of the millennium. . .no, those times were fairly predictable.

Even the pandemic was predictable; predictable in that just about everything shut down and employers and their workers simply had to adapt to survive. Millions of small businesses did not survive and some long-time employees chucked it all in and retired.

Who would have thought that an industry (data centers) that averaged 1.8 deals a year over 30-plus years (almost all in Virginia, then later Atlanta and Texas) would post nearly 80 massive projects in 2025, vaulting itself to No. 1 on the SB&D 100 list by a wide margin? In other words, data centers were as active as automotive and FIRE in their best years over the last four decades.

The rules have changed in economic development reporting

The rules have changed in every way. Now, some deals announced publicly are counting jobs to be created over a 10-year span. That’s misleading. The unwritten rule for decades was that jobs created for an announced project were limited to a three-year period.

That “rule” has been thrown out the window, mainly by politicians, who are also publicly announcing “spin-off” jobs, even with the inclusion of projections of retail projects that “could be” tied to the project. Again, B.S. Many governors today micro-manage their state economic development departments as a mechanism for political gain. It didn’t used to be that way.

So, as reporters, we must determine these things. After all, the SB&D 100 has rules and we are remaining steadfast in our reporting. If a project announces it will create 1,000 jobs over 10 years, we count those deals as 300 jobs in three years, but we “mention” the 1,000 “over 10 years.”

Here is a cinema angle of the rules

A.I.: “Smokey, this is not ’Nam. This is bowling. There are rules!” – Walter Sobchak, played by John Goodman, in the Coen Brothers’ classic film The Big Lebowski. He says it during a heated moment in a league bowling game when Smokey steps over the foul line.

So, let’s turn to A.I. to lead us to the rules because there are no “political leans” in artificial intelligence, at least not yet and we hope there never will be.

A.I.: “The number of servers in a data center varies drastically, from hundreds in small facilities (500-2,000) to thousands in average ones (2,000-5,000), and tens or hundreds of thousands (or even millions) in massive hyperscale data centers like those run by Google or Amazon. Key factors are size (square footage), purpose and density (servers per rack), with larger, modern facilities packing many powerful servers into each rack.”

One could point to data centers and their enormous use of resources, such as power and water, and say, “This is a gamble.” Well, it is. A trillion-dollar gamble.

But you cannot blame small communities in the South for capturing massive, hyperscale data centers. If A.I. doesn’t bubble, those communities will get rich. That statement was made by David Rumbarger, CEO of the Community Development Foundation at SEDR in December. If I recall, as of yet, Rumbarger has refrained from landing a data center. Tupelo is already rich.

But you cannot blame small communities in the South for capturing massive, hyperscale data centers. If A.I. doesn’t bubble, those communities will get rich. That statement was made by David Rumbarger, CEO of the Community Development Foundation at SEDR in December. If I recall, as of yet, Rumbarger has refrained from landing a data center. Tupelo is already rich.

Tell that to rural Haywood County, Tenn., north of Memphis, where a $5 billion battery and F-150 EV assembly plant has now been repurposed as Ford has ditched its Korean partnership with South Korean battery maker SK as a business venture. SK may one day still build batteries there.

Called the BlueOval City by Ford, the Detroit automaker is now renaming the massive plant the Tennessee Truck Plant, I guess similar to its Kentucky Truck Plant in Louisville. That plant, we have learned, will produce gas-powered and hybrid trucks starting in 2029, instead of electric vehicles; yes, the purest example of a bubble, but one with a likely solid landing.

Mark Herbison (Tifton County, Tenn.), the main dude in capturing that Ford plant in Haywood County, Tenn., said to the audience at SEDR a few years back (paraphrasing), “This has been built. It’s going to happen. There’s more than 5 million square feet of space out there. If it’s not EVs and batteries, it is too big to fail.”

Herbison was mostly right. You don’t build a $5 billion factory and let it sit for too long regardless of the EV bubble. Ford, as mentioned, will make it an F-150 assembly line. A gas one. A huge win! Just not as quickly as first announced.

More rules, as they are a-changin’

A.I. is as perplexing as when the internet was first widely used in the late 1990s. People saw the internet and domains coming, but they did not see the bubble early on. Or, the amazing benefits it would soon offer, like YouTube, Facebook. . .or, for that matter, email.

A more perfect example of the dot-com bubble can be found in SB&D’s next venture, almost 30 years later. I have been chasing the domain “SouthernBusiness.com” for all that time.

In 1997, Network Solutions priced the domain SouthernBusiness.com at $1.5 million. I have checked on the price off and on for decades. The domain was still priced at $150,000 in 2020. I bought it last year for $1,500 and we now own it and it is coming to a cell phone and computer screen near you soon.

We are retiring SB-D.com and the Southern Business & Development print product into one media property, SouthernBusiness.com, and y’all are going to go to it every single day. I promise you that. Instead of quarterly and monthly deadlines, SouthernBusiness.com’s deadlines will be daily.

“Reshoring:” The late Hal Sirkin of the Boston Consulting Group, Chicago

The “style” to describe the A.I. phenomenon is as convoluted as when the late Hal Sirkin of the Boston Consulting Group and I called the return of manufacturers from Asia to the U.S., “reshoring.” Sirkin was also the author of the book, “Made in America, Again,” which showed in great detail why manufacturers were leaving China and bringing their production back to North America.

Reshoring is perplexing in that Microsoft Word still does not recognize the word. Then again, the word was invented and first widely used in 2010. However, “offshoring” is a word, according to Microsoft.

It is as perplexing as the COVID years of 2020 and 2021. No one knew what to do then, even what to call it, but somehow we adapted and won that battle to a large degree.

Does anyone know what to do today, as the rules change every time the wind blows it seems. Some do, some don’t. Again, a dichotomy.

Are A.I. and electric vehicles a double bubble in this economy?

SB&D hosted an automotive summit event in Greenville, S.C., in the summer of 2024, at the height of those $250 billion investments in electric vehicles and battery manufacturing announcements made in the Southern Automotive Corridor. At the time, the CEO of the Michigan-based Center for Automotive Research, Alan Amici, told the audience, “This better work. There is too much money on the table for it not to work.”

Well, almost two years later, it hasn’t worked. Demand for EVs is rising, just not as fast as the investors expected. In other words, “Too much, too fast.” (See chart on page 42.)

Are the hundreds of billions already invested in A.I. a second bubble? While it is too early to tell, we do know that traditional stalwarts like automotive and financial services are AWOL on the big deal list of the 2026 SB&D 100.

Again, in a good economy, automotive and financial services soar in new projects. Not true in 2025. Too little, too late? Or are Trump’s policies too new and still in their infancy to materialize? That’s one of the dichotomies. Both may be correct in one form or another.

Morgan Stanley estimates that global investment in A.I. data centers and related industries could reach $3 trillion by the end of 2028

That figure is unheard of. That’s almost 10 percent of the U.S. GDP last year and 10 times what has transpired to date in total investment. And $350 billion has been spent so far in the South and in just one stinking year! This better work!

Morgan Stanley, the global financial services firm that provides investment banking, wealth management, investment management, and sales and trading services to corporations, governments and institutions, reports that global data center capacity will need to increase by approximately 10 times in the South and over six times in the U.S. in the next three years. That is just to support A.I. growth.

A.I. firms and their stocks, according to the British Broadcasting Corporation, have surged in the last year, “accounting for more than 80 percent of America’s economic growth.”

Wait, what? Eighty percent of America’s economic growth in 2025 has come from A.I., from one industry sector? Sounds like too much, too fast, huh? It should be noted that just about every traditional industry didn’t perform up to par in 2025. Too little, too late?

Data from the 2026 SB&D 100

Data from the 2026 SB&D 100

To review, for the first time ever, data centers led all industry sectors meeting or exceeding 200 jobs and/or $30 million in investment in the South. At the same time, financial services and the automotive industry have reduced their project totals dramatically compared to the last 33 years in jobs and investments meeting those thresholds. Our question is why?

While I have given an overview of how calendar year 2025 went for the South and the nation’s economy, simply put, almost all of it is not what we are used to. “Stability” is a word that cannot be used to describe 2025. But only as it compares to the last 33 years. As mentioned, the word used the most was “uncertainty” by the media, including us.

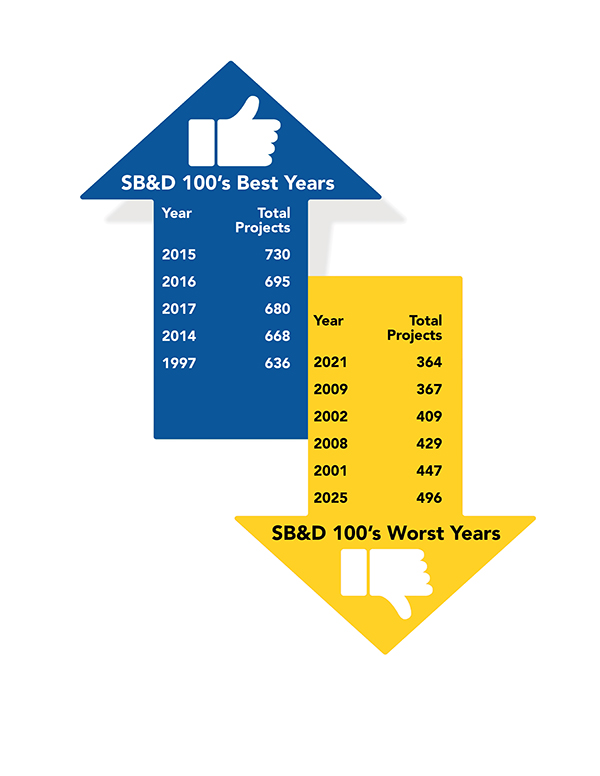

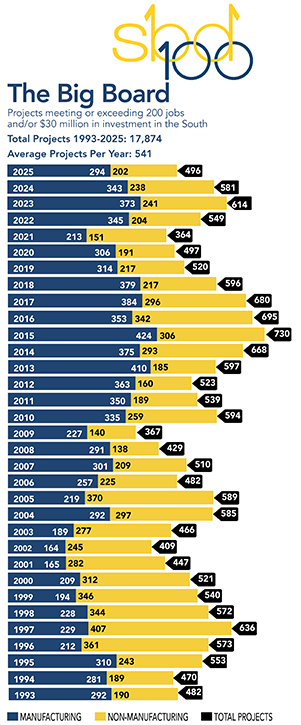

Therefore, in terms of corporate and industrial project counts meeting or exceeding our thresholds, 2025’s numbers were not only down, they were down significantly.

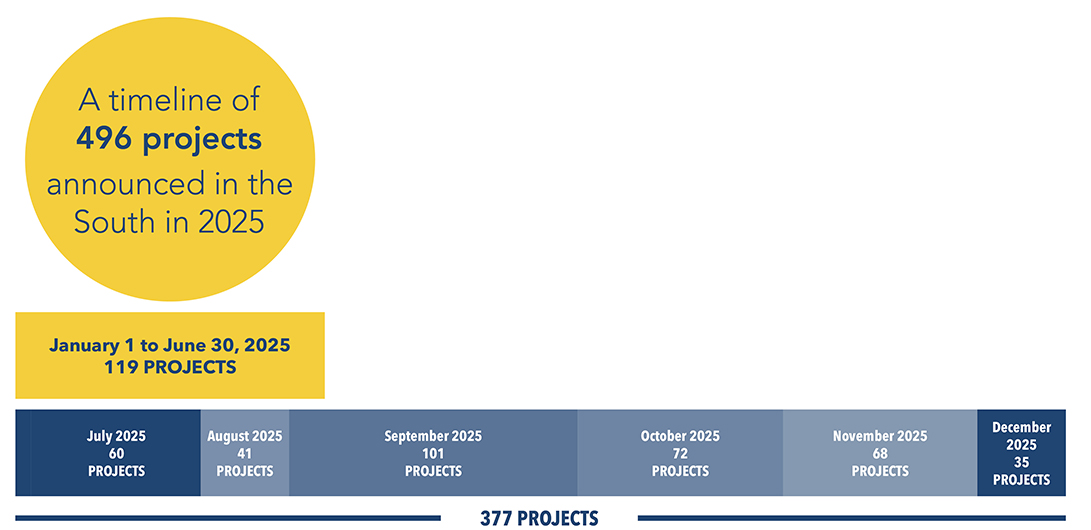

I wrote a story mid-year about the shockingly low number of projects after the first two quarters of the year. In the first six months of 2025, only 119 projects were announced in the South meeting or exceeding our thresholds. This was most likely a response to “Liberation Day,” as President Trump called it (April 2, 2025) when tariffs were announced, many of which bounced up and down on a regular basis the rest of the year.

Those awful totals for the first six months were turned around the second half of 2025 as we just missed 500 projects announced. Without almost 80 data center deals announced, it would have been a year similar to those during and shortly after the Great Recession.

Then again, a total of 496 projects last year is right at the mark set during the COVID year of 2020, so certainly totals not worth writing home about.

Then again, a total of 496 projects last year is right at the mark set during the COVID year of 2020, so certainly totals not worth writing home about.

In fact, by averaging all 33 years of the SB&D 100, 2025 was 46 projects below a typical year. Without data centers, 2025 would have mirrored the recession years of 2008 and 2009 (429 and 367 deals, respectively), as well as the recession of 2001 and 2002 when just 409 deals were turned.

In fact, by averaging all 33 years of the SB&D 100, 2025 was 46 projects below a typical year. Without data centers, 2025 would have mirrored the recession years of 2008 and 2009 (429 and 367 deals, respectively), as well as the recession of 2001 and 2002 when just 409 deals were turned.

Conclusion

Conclusion

While 2025 wasn’t a total cratering of big deals announced in the South, it was certainly not a good year. It was a bit below average when the year started off as a disaster. The two stalwarts of industry in the South, financial services and the automotive sector, simply sat on the sidelines.

The real canary in the coal mine is the lack of financial services deals. Those folks are smart. They can predict the future better than any other industry (other than automotive).

The automotive industry knows the “standard economy” better than any based on our experiences of economic development journalism for four decades. Then again, today’s economy is far from standard.

Yet, this is a new day — a “real new day” — if you read the great economist Mark Vitner’s comments he made at SEDR@RosemaryBeach in December and repeated in this story.

No doubt there is a new sheriff in town. And that sheriff is President Trump and his new and. . .what is the word again?. . .“distinct” or “incomparable” economic policies.

We don’t discuss “politics” at SEDR, mainly because political hate is so prevalent. But, we certainly do discuss economic policy among the finest economic and economic development minds in the South.

On a smaller scale, it is akin to someone taking a local or statewide economic development leadership position from another who had worked for decades with great success, only to throw out that template like the “baby with the bath water” to implement his or her system of recruitment and marketing. Sometimes it works, sometimes it doesn’t.

Believe me, after almost 50 years of owning this media company, we have seen both situations where ditching a proven system to implement another is chancy at best.

Or maybe the old one was getting stale?

A tipping point? There is so much on the line.

Throw in geopolitical tensions regarding trade that seem to be heightened each month, the South and the nation’s economy are at a tipping point. And that tipping point is focused on a single industry — A.I. — propping up an economy that is more than slow, it is “conflicting.”

Consumerism is “conflicting.” But without it and A.I., where would be after 2025? The poor and middle-class are buying less. The upper middle class and rich are buying more.

So, not unlike the introduction to this story, the economy is “conflicted.” Economic data appears “conflicting” because different parts of the economy are moving in opposite directions.

In short, the rich got richer in 2025 in the South and according to the data, the poor got poorer and the middle class squeezed.

It goes back to the age old question. . .are we better off with top-down economics or bottom-up economics? J

Sources for all data: SB&D, Southern state economic development agencies, other media sources. SB&D’s coverage area includes: AL, AR, D.C., FL, GA, KY, LA, MS, NC, OK, SC, TN, TX and VA.

Southern Business & Development

8086 Westchester Place

Montgomery AL 36117

205.871.1220

| SECTIONS | MAGAZINE | OTHER NEWS |